- Pricing

- Mentorship

-

Private Company Valuations—A Complete Guide

- About Us

- Contact

- Log In/Sign Up

- VIP

Private Company Valuations—A Complete Guide

The market approach is a commonly used method for determining the value of an asset by analyzing the selling prices of comparable assets. This approach is one of three widely recognized valuation methods, alongside the cost approach and discounted cash-flow analysis (dcf).

Irrespective of the nature of the asset in question, the market approach involves analyzing recent sales data of similar assets and adjusting account for any differences between them. For instance, when evaluating real estate, adjustments may be made based on factors such as the size of the property, the age and location of the building, and its amenities.

The market value approach in business valuation involves assigning a value to a business based on market forces in comparable situations. These situations may include a prior transaction involving the same business, an ownership transfer transaction with a comparable (public or private) company, or a market quote of listed securities of a comparable public company.

The primary advantage of the market value approach lies in its reliance on publicly available data from comparable transactions, reducing the need for a high number of assumptions compared to other valuation methods. Utilizing the market value approach for business valuation is particularly appropriate in the following scenarios:

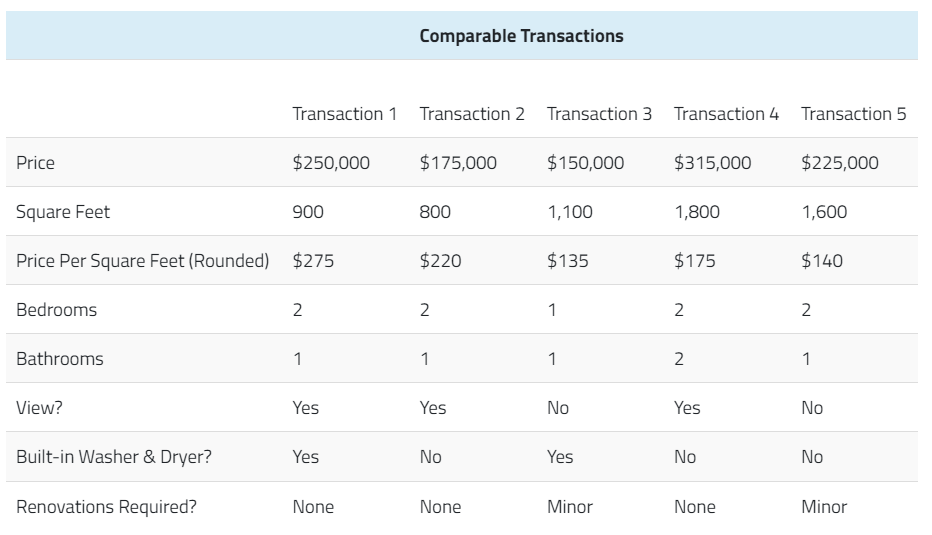

Let's consider a real estate scenario to better illustrate this methodology. Assuming you are in the market for a new apartment, you come across a listing for a 1,000 square-foot apartment with one bedroom and one bathroom in your desired neighborhood, priced at $200,000. While the apartment is in good condition, it requires some minor renovations and lacks certain amenities such as a built-in washing or drying machine. Despite its location, you believe the asking price is too high, especially given its limited view.

After the listing has been on the market for over a month, you decide to negotiate with the seller. To determine a fair market value for the property, you research similar apartments in the area. By analyzing comparable transactions, you find that apartments in the neighborhood have sold for prices ranging from $135 to $275 per square foot. Properties at the higher end of this range typically offer more amenities and features, while those at the lower end may require renovations.

In comparison, the apartment you are interested in is priced at $200 per square foot and lacks some of the desirable features seen in higher-priced units. Based on this information, you believe a lower offer is justified. After careful consideration, you make an offer of $150,000, which is accepted by the seller.

Having established an understanding of the market value approach in business valuation, let us now explore the various types that exist. There are numerous classifications within this approach, depending on the origin of the known values utilized as reference points. However, our focus will be on discussing the two primary types that are most commonly employed. These include:

In conclusion, the market value approach is a key method for business valuation. It can provide valuable insights into the worth of a company, particularly when comparable firms are available for comparison. It is important to note that for small sole proprietorships, alternative valuation methods such as the income-based approach may be more suitable.

EQTBLOOM

Vatsalaya Rasa Private Limited

Address: WZ 1324 Rani Bagh Delhi 110034

Email: contact@eqtbloom.com

Phone: +91 9711003475

Copyright © EQTBloom 2024